Original content by David King, DVM, CVA, revised by David McCormick, MS, CVA 5/2024

We often hear that rising educational debt means that recent graduates cannot buy a veterinary practice. Fortunately, this is not the case.

The only effect of educational debt on a practice loan application is the size of the monthly payment and its impact on a buyer’s after-debt income.

The lack of extra income scenario may be true when it comes to buying a car or a house, but usually not when buying a practice. That’s because in the case of a car or a house, YOU have to pay for it out of your household income. When buying a practice, the practice profit pays for the practice. You do not use your household income.

An Owner-Operator of a Veterinary Practice Receives Four Potential Benefit Streams

- Compensation for being a veterinarian. If you produce a lot, you get paid a lot. This goes to your household whether you are an associate or an owner.

- Compensation for the time spent managing the managers, overseeing the bookkeeping, and strategic planning. This macro-management/leadership compensation goes to the owner.

- If you purchase the real estate, the practice is a tenant and the tenant pays you a rent. This rent pays the real estate mortgage.

- The profits from owning a business go to the owner.

The above is the total cash flow after all of the practice’s operating expenses have been paid but before servicing the debt and paying taxes.

When it comes to buying a practice, veterinary lenders rely on the “Three C’s” when approving a loan.

The “Three C’s” of Veterinary Practice Loans

Credit

Your credit score is a reflection of making timely payments on the debt that you currently have and how you have managed debt in the past. If your FICO score is between 650 and 700 or higher, you are usually able to borrow for a practice acquisition. If it is lower and there is a reason, there are specialty lenders that may still be able to help.

Character

This relates to almost everything else in life – how you manage your money, how you have been preparing for becoming an owner, being a licensed veterinarian, not having a criminal record, etc. Once a potential buyer gets past the “Credit” and “Character” hurdles, it becomes all about the practice.

Cash flow

This is the pile of money mentioned above. The veterinary lenders look at the practice’s cash flow, then subtract the salary needed to support the buyer’s current lifestyle and personal debt service.

They also subtract a modest safety margin amount, and then they subtract the amount required to service the practice loan. If the remaining amount (e.g. the after-debt cash flow) is a positive number, the loan will likely be approved.

In other words, veterinary student debt will not prevent you from buying a practice because servicing your student debt comes from your veterinary compensation.

Having student debt might influence the size of practice you purchase. A smaller practice may not allow you to produce enough to receive enough doctor compensation to cover your household expenses which include your veterinary student debt. This means that you may need to target a larger practice – or a smaller practice that can be rapidly grown.

Also keep in mind, that as part of your monthly veterinary practice loan payment goes towards the principal, you are building equity in the practice. While you cannot spend this in the same manner as take-home pay, it does increase your net worth.

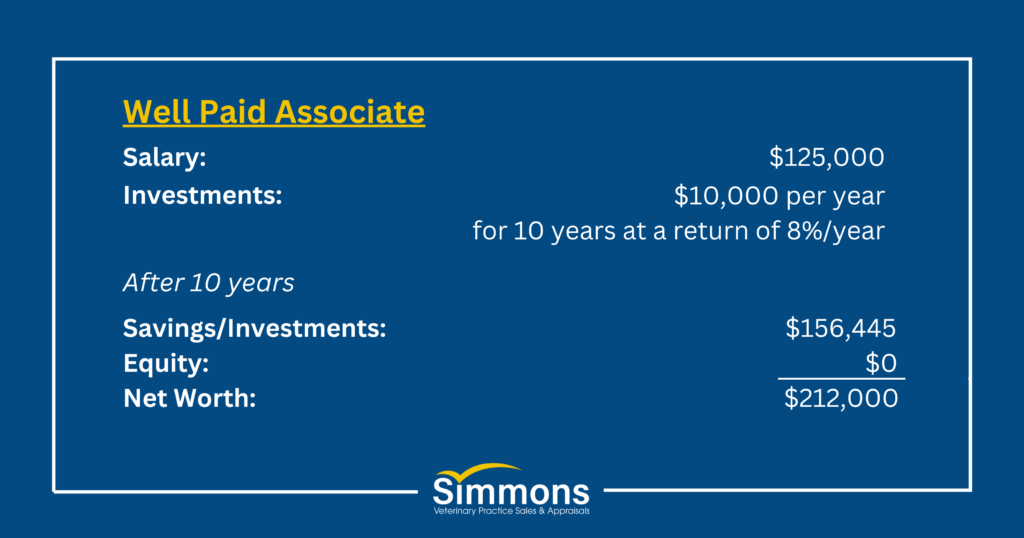

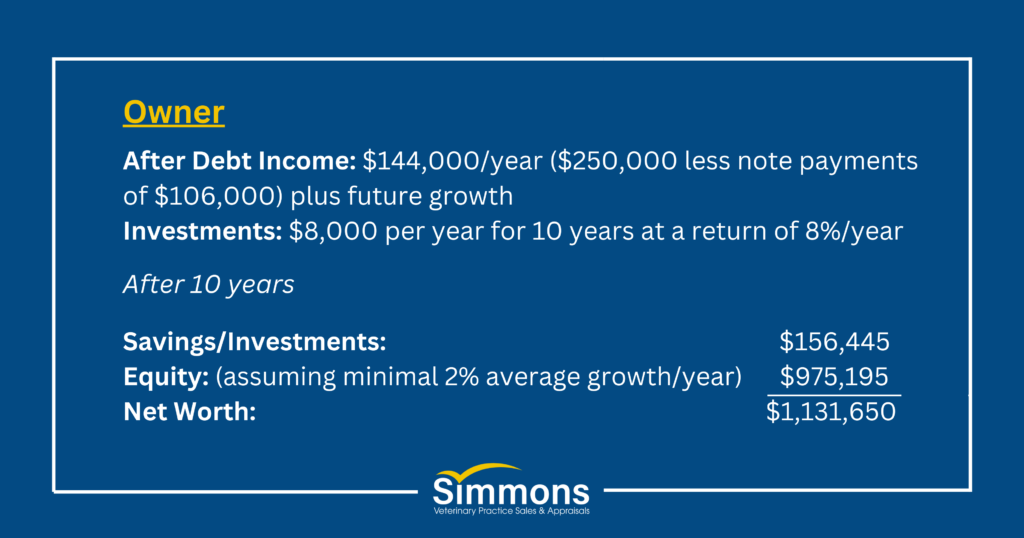

Let’s say you are an associate making $125,000/year and you manage to pay your bills (including your debt) plus tuck away $10,000 into a retirement fund (nice job BTW). You invest well and are getting an 8% average return on this investment (again nice job). You are considering buying a practice for $800,000 (note terms of 6% for 10 years) that is grossing $1,000,000 and has owner cash flow of $250K.

Your decision is whether to stay an associate or jump into ownership. Look into the future after the loan is paid in full and it might help you decide. It could look like this:

While making money is not the reason most doctors become owners, the ownership path does look good financially. Also keep in mind that when the veterinary practice loan is paid off after 10 years, then the $106,00 in loan payments is now coming to you, not the lender. That is $250K without any growth and you are a millionaire! (– and you had the extra cash to pay off your student loans.)

Overcoming Veterinary Student Debt Through Practice Ownership

The ever-growing student debt is definitely a problem for our profession. Ultimately a solution will require someone higher up the food chain than most of us. Meanwhile, all we can do is play the cards that we’re dealt and that means trying to earn as much income as possible to retire the student debt, and provide for those we love.

Practice ownership is just one path. It is important to know that student debt is not an impossible obstacle to practice ownership – and that practice ownership can be a solution to the burden of student debt.

This article was originally posted on www.simmonsinc.com. Any reproduction on any other site is prohibited and a violation of copyright laws.