This article was co-authored by David King, DVM, CVA and Kate Owens, DVM, MBA, CVA.

You might be surprised to learn this truth, but practice value is NOT a function of gross revenue.

Rather, two main components create practice value. One is profit and the other is risk/desirability.

Most valuations are done to arrive at what is known as Fair Market Value. This is the value of the practice if put on the open market to the average buyer. A full definition is, “the cash or cash equivalent price at which a practice would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of the relevant facts and after having been exposed to the market a reasonable length of time.”

How is Practice Fair Market Value Determined?

The basis of value is profit. ALL high-value practices have high profits, but not all high-profit practices have high value. This is due to intangible elements (risk/desirability) like location, quality of staff and facility, services offered, etc. But, the place to begin is profit.

True profit is figured by converting the tax-based accounting documents to management-based ones. This is done by removing unnecessary expenses, one-time expenses, adjusting spousal and owner’s salaries (up OR down) to their fair market level, etc. In short, the true profit is the amount of money left over after subtracting from gross revenue all of the normal operating costs (owner’s compensations and rent ARE normal operating costs and NOT part of profit).

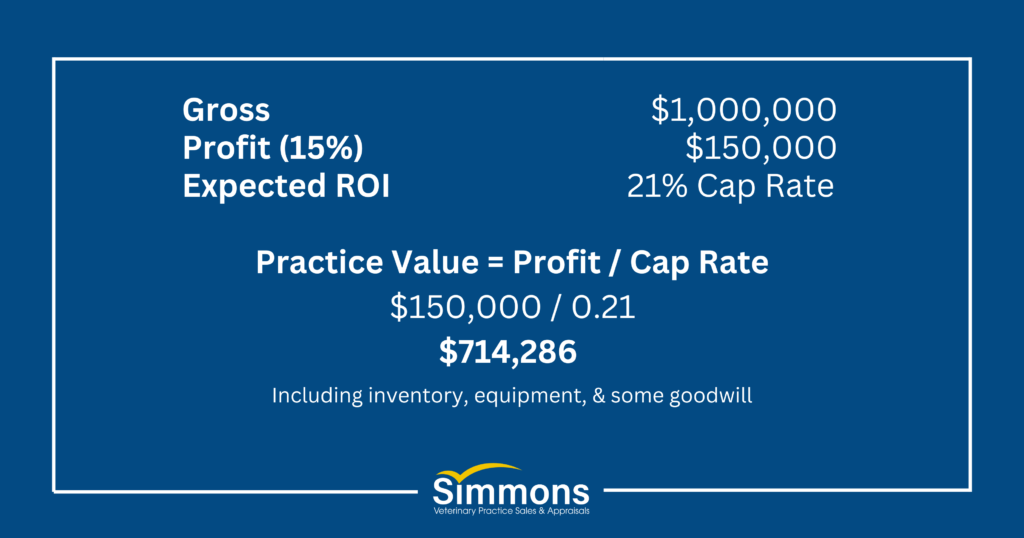

Then this remaining amount (profit) is capitalized. Capitalization of profit is the amount of return the average investor expects to receive on an investment annually, with the investment being the value of the practice. So, if the average investor expects a 21% return (since veterinary practices carry higher risk than large, publicly traded companies or a savings account), that profit represents 21% of the practice value. Let’s look at an example:

A capitalization rate is also the expected rate of return or ROI. A less favorable, more risky practice with a high rate (ex. 35%) means you pay less and as a result get a better ROI than if that same practice had a lower capitalization rate (lower expected ROI).

How is Veterinary Practice Profit Figured?

Profit is NOT the bottom-line number on the tax return that shows “net income”. Since tax returns are generally designed to minimize taxes, they typically do not reflect the true profit of the business, and adjustments are required. Most owners do not pay fair market wages and rent to themselves to minimize taxes and therefore these expenses are a common adjustment in the valuation process. An owner should be paid the following:

- Salary as a producing doctor

- Salary as a manager

- Rental income if he/she owns the facility, and, finally, what is left over is…

- Profit

It is the profit that is used as the basis of practice value.

EXAMPLE:

Assumptions:

- Gross revenue $1,000,000

- Owner produces $450,000

- Production salary is 22% of personal production

- The building is valued at $1,500,000

- Fair rent for the area is 8% of building value

- Management compensation is 3% of gross

- The owner takes home a total of $325,000

How much is the profit?

| TOTAL | $325,000 | |

| Doctor salary | -99,000 | (450,000 x 22%) |

| Rent | -120,000 | (1,500,000 x 8%) |

| Management pay | -30,000 | (1,000,000 x 3%) |

| TRUE PROFIT | $76,000 |

It is this true profit number that is used as the basis of value. Sometimes only the most recent year is used, but, more often, the last 2-3 years are examined to look for trends and to smooth unusual years. Remember, a practice valuation is an attempt to provide the best predictor of the future performance of that business by examining the past. If multiple years are used, a “weighted average” is often considered to be most accurate. A weighted average gives the most weight to the most recent, and less to previous years, the reasoning being that the most recent year is the best predictor of the future. Of course, that is not always the case.

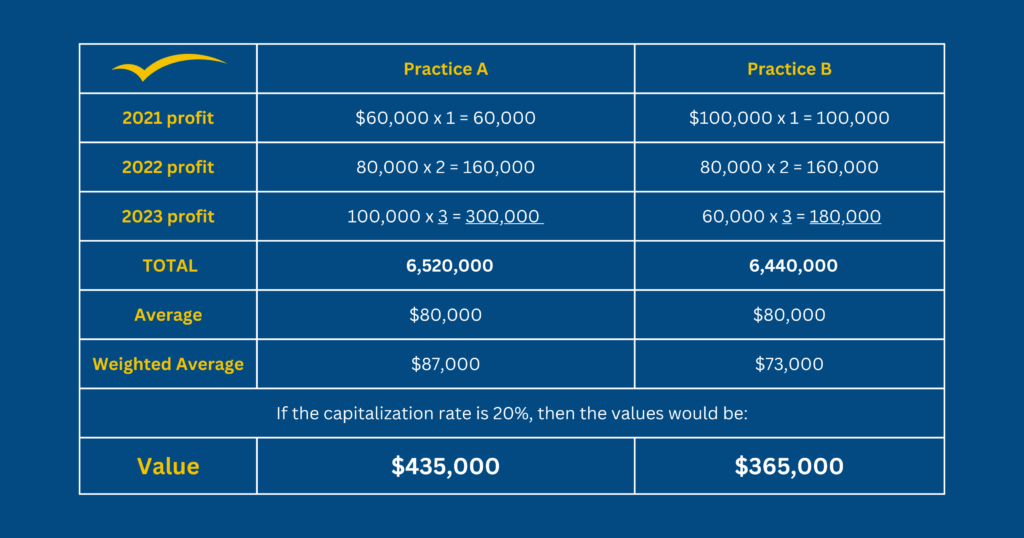

Example: Which practice has a higher value (assuming equal risks)?

These two practices have the same average profit over the past three years, but practice A has increasing profits whereas practice B has decreasing profits resulting in different weighted averages. The practice with increasing profitability has a higher practice value than the practice with decreasing profits after capitalizing the weighted average.

How Do I Choose a Capitalization Rate?

This is where art and science merge. There is an expected financial “return” anticipated when acquiring an investment. The “rate of return” of this investment is primarily a function of the risk inherent in the investment. The rate of return becomes the capitalization rate. The capitalization rate is then applied to the profit of the practice, which converts the financial return to practice value. In our profession, we also include the desirability or marketability as part of the capitalization rate.

For example, the 20-year US Treasury Bonds are considered VERY low risk, but as a result, their return is also low, usually around 4.6%. Conversely, small businesses such as veterinary practices are considered to be riskier and, as a result, the expected rate of return is necessarily higher. The vast majority of veterinary practices have risk factors (capitalization rates) of 18% (very favorable ⇨ high value) to 35% (not so favorable ⇨ low value), with a few exceptional situations.

So, what makes the cap rate 18%, or what makes it 35%? Many factors should be considered and this is where the “art” of valuation enters in and why valuators may arrive at different values even if their calculation of profit is the same.

Below are some of the factors that should be considered when arriving at an appropriate capitalization rate.

Practice growth contributes an intangible value, as does geographical location. Tangible asset value is the value of the equipment and the inventory. However, it is income that buyers want, not “stuff”, so the equipment value doesn’t play as important a role as might be expected. Of course, certain equipment is necessary, but too much equipment or very expensive equipment does not increase value.

Long-term, loyal, skilled employees add value, as does a reasonable transition period by the selling doctor. A multi-doctor practice, where the associates remain post-sale, will have more value than a solo-DVM practice where the selling doctor leaves on the day of the sale. A small, “high touch, boutique” practice has more loyal clientele than does a high volume, “low cost” practice. A practice in a permanent location as opposed to a mobile practice will have more transferable goodwill because the clients will more easily remain with a fixed-location practice, hence, more value. And, what about competition? Is it more advantageous to be in a market with several other practices or few? The answer is not as simple as it sounds.

What about a new housing development under construction? Is a practice in Detroit more risky than one without any influence from the auto industry? Is there a new freeway planned that will increase or decrease access to the hospital? What about visibility? Is it anticipated to get worse? Can the hospital be expanded for future growth, or are there zoning restrictions? Is the economy diverse or single sector?

All of these things are elements of risk/desirability that have an influence of value, and, yet, don’t show up on the financial statements. If the risk of maintaining the current level of profit is greater in one practice than another, even though the profit is the same right now, its value will likely be lower.

What’s the Difference Between a Capitalization Rate and a Multiple?

You may have heard a friend or colleague mention they got a 6 multiple (or much higher from a corporation) when they sold their practice. But how does a multiple relate to the capitalization rate? The multiple is the inverse of the capitalization rate. For example, the 20% capitalization rate from the above example would be the same as multiplying the profit by 5 (1/.20 = 5).

The less favorable the practice, the higher the capitalization rate (35%, for example) and lower the multiple (2.8). Likewise, the more favorable the practice, the lower the capitalization rate (18%) and higher the multiple (5.5).

Corporate Sales and Capitalization Rates

We have been discussing fair market value and capitalization rates, but how do corporate offers compare to this? Corporate consolidators do not value practices on fair market value but use investment value instead. Investment Value is defined as “the value to a particular investor based on individual investment requirements and expectations”. Their capitalization rates are much lower (or multiples much higher) than a fair market valuation because they are considering their investment requirements, expectations, and the synergy they will have between their corporation and the acquired practice. It is also worth noting that investment capitalization rates have increased over the past 12-18 months; while many 4-6% rates (16-25 multiples) were seen in 2020, it is more common to see 8-13% (8-12 multiples) today.

They will also likely have a different profit calculation than a fair market valuation. A corporation will adjust not only the owner’s salary, rent payments, and one-time expenses but they will also adjust their known expenses going forward. This can include their cost of goods sold, usually lower, or employee benefits, usually higher, than the practice’s current expenses.

The high corporate values over the past several years have begun to affect the private sales market. A private investor (veterinarian) cannot invest in a practice at the investment value (corporate price) because the debt service on the purchase would result in bankruptcy in the first year. The investment values being paid though are showing the veterinary market is less risky than previously thought and it is bringing down the overall capitalization rates of the industry. So, while fair market capitalization rates and values will never be the same as investment capitalization rates and values, they are getting closer as investor rates go up and fair market value rates come down.

Conclusion

Practice valuation, much like veterinary medicine, is a science and an art. It is crucial to have your valuation performed by a qualified valuator who has experience in the veterinary field. Look for a Certified Valuation Analyst (CVA) or a Certified Business Appraiser (CBA) and ensure they specialize in veterinary practice valuations. While it isn’t as easy as a percentage of gross revenue, it is easy to understand once you know the basics. You don’t need to be Sherlock Holmes to unravel the mystery of a practice valuation.